Australia has a strong hand. Are we playing it well?

Key findings

1. Housing supply is not keeping up with demand

Rapid rental price growth has contributed to the cost-of-living crunch facing Australian households, with the impact concentrated on low-income households. CEDA analysis estimates that renters among the poorest fifth of Australian households could be paying an average of 44% of their disposable income on rents in 2023-24, based on a 20 per cent increase in asking rents from 2021-22 as of February 2023.[i]

A key driver of rapid rent increases has been the lack of housing stock available for rent. National rental vacancy rates have hovered at close 1 per cent during 2023, well down on the pre-pandemic decade average of 3.3%.[ii] Capital city rental vacancy rates reached a record low in early 2023.[iii]

Demand for housing space has increased due to two factors – reduced household size and increased population. Declining average household size between 2020 and 2022, driven by a desire for more household space as working from home increased, is estimated to have increased the number of households (and thus demand for dwellings) by 120,000.[iv] The return of immigration has now further boosted housing demand: Australia’s population growth reached a record high of just under 500,000 annually at the end of 2022,[v] requiring roughly 200,000 additional dwellings per year based on the national average household size.

At the same time, housing construction activity has cooled, with new dwelling commencements of 180,000 in the year to the March quarter of 2023. This represents a decline of more than 20% from a year earlier and is well below the annual average of 210,000 in the five years preceding the pandemic.[vi]

2. There is a lack of institutional investment in rental housing

A contributing factor to the slow growth in housing supply is a lack of institutional investors in the Australian market. Institutional investors currently play a small role in the Australian market for rental housing, with the largest investors only holding a few thousand units. In Germany and the US, by contrast, the largest institutional investors hold a combined total of more than half a million dwellings.[vii]

By mobilising investment capital, institutional investment offers the potential to increase stocks of rental housing. Increasing institutional investment in rental housing can also benefit renters through greater tenure security, as occupants are less likely to be evicted for reasons separate to the renter, such as the owner or their family moving in.

Institutional investors face tax disadvantages relative to individual owners in Australia due to the structure of land tax, which is levied in a progressive fashion on the total value of non-own-home land holdings and thus favours holders of few properties. Negative gearing, where annual losses can be offset against unrelated income, is less advantageous for institutional investors than for individuals paying top marginal tax rates.

These incentives against institutional investment are particularly strong for houses, where they are magnified by high land values and low rental yields.[viii] A further tax disadvantage for institutional investors historically has been the 30 per cent withholding tax on managed investment trusts; the Government’s decision in the 2023 budget to reduce this rate to 15 per cent for newly constructed build-to-rent developments is therefore welcome.

3. The supply of social housing has not kept up with population growth

Social housing can play a vital role as a safety net for those who are not well-served by private rental markets. There has been little change in the number of social housing properties since the Social Housing Initiative ended in 2012. In 2021, more than 160,000 households were on a wait list for public housing. Supply has not been keeping pace with population growth[ix] and the current shortfall poses a risk of more Australians falling into precarious housing situations.

Since social housing has a strong protective effect against homelessness,[x] the failure of supply to keep up with population growth is a contributing factor to the increase in homelessness between the 2011 and 2021 censuses and the 18 per cent increase in people seeking support from specialist homelessness services between 2011-12 and 2020-21.[xi]

4. There is a mismatch between housing size and household size

For a given supply of housing, there can still be rental shortages if supply is not well-matched to demand. This can be due to spatial mismatch, where dwellings are not in the same places that people want housing, but also mismatches between types of dwellings and the households living in them.

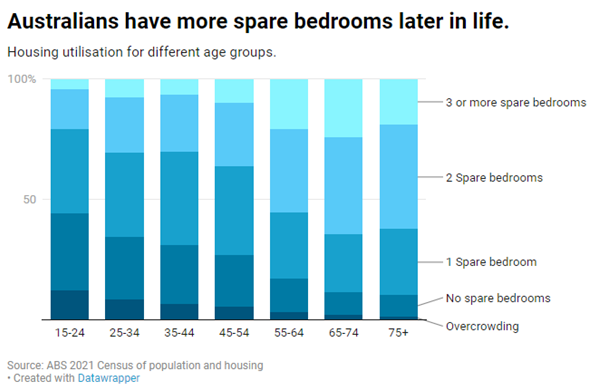

There is evidence of increasing mismatch, as people age, between the number of bedrooms they need, based on the number of people in the household, and the number of bedrooms where they live (Figure 1). This is not surprising: as people get older household sizes decline, particularly as children grow up and move out. However, mismatch is exacerbated by policy settings that encourage households to stay in larger houses through increasing the cost of moving home (notably stamp duty). The exclusion of the family home from the asset test to receive the age pension can also lead some older people to remain in a larger home than they need, rather than downsizing and potentially losing access to the pension due to an increase in non-housing assets.[xii]

Figure 1

5. Renting is often not a viable long-term option

The lack of tenure security for Australian renters undermines the role that renting can play as a viable long-term option for many Australians. Private renters comprise around one third of households in Australia and move roughly four times as frequently as owners and more than twice as frequently as social housing tenants.[xiii] Across 27 OECD countries, private renters move more often in Australia than in any country except Iceland.[xiv]

Lack of security of tenure is a key contributing factor to high mobility of renters: more renters are forced to move by their landlord than choose to move for work or study.[xv] In the United States, by contrast, eviction rates are far lower and non-public-housing renters are ten times more likely to move for a new job or transfer than due to eviction.[xvi] Long-term leases are rare in Australia (for housing – multi-year contracts are far more common for commercial leases) and renters live with constant uncertainty about whether they will have to move, particularly as the overwhelming majority of landlord terminations are for reasons entirely separate to the renter.[xvii]

Overall tenure security for Australian renters is ranked equal lowest (along with Greece) among 31 OECD countries for which data are available.[xviii] Compared with other developed countries, Australians are also relatively constrained in their capacity to make minor alterations to rental properties.[xix]

Benefits of secure tenure include improved connections to community, better health outcomes and higher levels of social and economic participation.[xx] Stable and secure rental tenure is protective of mental health, with average mental health of private renters lower than that of comparable homeowners until five-to-six years of tenure, when the difference becomes indistinguishable.[xxi]

The worsening rental crisis

23 August 2023

CEDA Senior Economist Andrew Barker's comments to the Community Affairs Reference Committee

Key recommendations

1. Accelerate supply through planning reform, encouraging institutional investment and investing in social housing

Housing supply needs to be addressed through multiple levers, including planning reform, encouraging institutional investment and more direct investment in social housing. As set out in CEDA’s submission to the Employment White Paper,[xxii] planning and zoning restrictions should be relaxed to allow higher density development in appropriate locations. Land-use rules are necessary to prevent inappropriate development and protect community values, but restricting development means more housing is needed elsewhere, often further from city centres where infrastructure is not as well-developed, exacerbating congestion.

Growth-accommodating reforms to planning arrangements are a crucial part of addressing barriers to increased housing supply and have a statistically significant positive effect on housing supply. For example, upzoning and relaxed land-use regulations in Auckland in 2016 added around four per cent to the city’s housing stock in subsequent years and saw rents grow more slowly than in the rest of New Zealand.[xxiii] By allowing higher density development in inner areas and transport corridors, such development can also boost productivity through shorter commutes. Improved clarity and defined timelines for development approvals are also important to reduce risk for developers, enabling them to ramp up production when economic conditions are favourable.

Planning practices that constrain development of medium-density housing are widespread, such as bans on townhouses in low-density residential suburbs that make up large parts of Brisbane and Sydney. Restricting development has important distributional consequences, contributing to higher house prices and rents that benefit wealthy owners of multiple properties at the expense of first home buyers and renters. Strict land use regulation can thus drive greater segregation between wealthy and low or middle-income households.

Building a stronger market for institutional investors in rental housing could help improve the availability of rental housing, for example via “build to rent”. It also has potential to increase tenure security, by reducing eviction due to the owner’s personal situation, for example if they need to sell the property, or if they or a family member wish to move in.

There is currently an opportunity for institutional investors as yields rise and land values fall, particularly build-to-rent investors who benefit from land-tax discounts in NSW, Victoria and Western Australia. This opportunity could be enhanced by flattening the payment schedule for land tax and reforms to reduce the importance of negative gearing. The US, for example, has a vibrant build-to-rent market and only allows individuals to make tax-loss write-offs against other forms of passive income (i.e. not against wage income).

Overcoming the barriers to unlocking institutional investment in affordable and social housing can also contribute to supply. Collaboration and partnership across the public, community, and private sectors, underpinned by firm funding commitments and viable delivery mechanisms, has the potential to improve the residential housing stock while supporting skills and capacity building across the housing industry. Case studies in Australia and internationally demonstrate that there is private sector appetite and capacity to deliver affordable and social housing, and that there can be positive outcomes where incentives are aligned between partners.[xxiv]

A more direct boost, jointly funded between federal and state governments, is also needed to increase social-housing stock and improve outcomes for the most vulnerable. New stock must address the need for smaller units: most social housing households are single adults, but only 26 per cent of the stock is one-bedroom or a bedsit, as it was built to meet different needs historically.[xxv] Social housing builds can also provide a reliable pipeline of building activity, softening cyclical fluctuations in private-market activity. This can ensure skilled workforces and industry capacity are retained during downswings.

2. Encourage better use of existing housing through stamp duty reform

While the choice of where to live must remain an individual decision, reducing policy barriers to moving into more suitable housing, particularly for older Australians, could free up some of the existing housing supply. Such reductions in housing mismatch would have benefits for first home buyers and renters.

Stamp duty is a highly inefficient tax that, as a transaction tax, restricts downsizing by older homeowners.[xxvi] Stamp duty is also a volatile source of revenue that is difficult to forecast and subject to property market volatility. Its importance for state and territory revenues has increased over time as house prices have soared.[xxvii] In NSW alone, replacing stamp duty with land taxes is estimated to boost long-term incomes by $10 billion by enabling people to move to homes that better suit their lifestyle, and by making it easier for people who move for work or for family reasons to access the property market.[xxviii] By reducing dwelling prices and purchase costs, replacing stamp duty with an annual broad-based property tax would also enable hundreds of thousands of households to shift from renting to owning their own home.[xxix]

3. Provide greater security of tenure for renters

Greater rental security should be pursued by removing landlords’ capacity to evict tenants without cause.[1] While some jurisdictions have made reforms in this direction in recent years, it is still possible to evict tenants without grounds at the end of a fixed-term tenancy (with a minimum 30 days or less of notice in NSW, Western Australia, South Australia and the Northern Territory) or by demanding a disproportionate rent increase. Although tenants can dispute a rent increase if they think it is excessive, in practice this is complicated as it requires comparison of rents with similar properties.

Regulations that control rental prices across-the-board carry significant economic costs, but there can be benefits from simple metrics to regulate price increases for existing tenants. By pushing returns below market rates, rent control holds back the supply of new housing[xxx] and works against mobility by locking people into favourable arrangements.[xxxi] Equally, however, once tenants are already living in a property, they can be in a situation of “economic hold up” and vulnerable to excessive rent increases where they do not want to move away from work, school, family or friends. A solution would be only to allow rents on existing tenants to be increased in line with a local measure of rental prices (with allowance made to recoup expenditure on major renovations). Such an approach in Germany has maintained a link with market rents without forming a barrier to investment.[xxxii]

4. Support low-income households through better targeting of Commonwealth Rent Assistance

Rental affordability should also be addressed through a review of the role and rate of Commonwealth Rent Assistance (CRA). CRA is a valuable way to support renters without dampening mobility, as it is fully transferable. However, it is indexed to the Consumer Price Index rather than rents, so does not automatically keep up with rapid increases in rents – relevant recently as rents for new tenants increased by over 20 per cent over 2021 and 2022.[xxxiii] The Government announced in the 2023/24 Budget that it will increase the maximum rates of Commonwealth Rent Assistance by 15 per cent. While this is welcome, it would be preferable to build-in either regular reviews or indexing directly to national rents.

Reforming CRA eligibility rules to better reflect housing need could substantially improve affordability while generating cost savings.[xxxiv] Improving targeting would also minimise the extent to which higher payments would raise rents through increased demand. There would also be benefits to assessing the best mix of funding allocations between CRA and social housing.[xxxv]

References

[1] Acceptable reasons for eviction include the owner or their immediate family moving in, sale to another owner who wishes to move in, or breaches/notice of intention to leave by the tenant.

[i] Andrew Barker, “The Cost-of-Living Crunch Is Set to Hit Many Households Hard in 2023,” Opinion Article (CEDA, 2023), https://www.ceda.com.au/NewsAndResources/Opinion/Economy/The-cost-of-living-crunch-is-set-to-hit-many-house.

[ii] CoreLogic, “Quarterly Rental Review Australia: July 2023,” 2023, https://content.corelogic.com.au/l/994732/2023-07-05/z2tcd/994732/1688600749Ly8Iv9wt/202306_CoreLogic_RentalReview_July_2023_FINAL.pdf.

[iii] PropTrack, “Rental Report: March 2023 Quarter” (Brisbane, 2023), https://rea3.irmau.com/site/pdf/85724293-2285-4c8a-9c91-463f515c364d/PropTrack-Rental-Report-March-2023.pdf.

[iv] Nalini Agarwal, James Bishop, and Iris Day, “A New Measure of Average Household Size,” Bulletin - March 2023 (Reserve Bank of Australia, 2023), https://www.rba.gov.au/publications/bulletin/2023/mar/a-new-measure-of-average-household-size.html.

[v] ABS, “National, State and Territory Population,” 2023, https://www.abs.gov.au/statistics/people/population/national-state-and-territory-population/latest-release.

[vi] ABS, “Building Activity, Australia,” 2023, https://www.abs.gov.au/statistics/industry/building-and-construction/building-activity-australia/latest-release.

[vii] Martin, C., Hulse, K., & Pawson, H. (2018). The changing institutions of private rental housing: an international review. AHURI Final Report No. 292.

[viii] Andrew Barker and Sebastian Tofts-Len, “Employment White Paper Submission,” 2023, https://www.ceda.com.au/ResearchAndPolicies/Research/Workforce-Skills/Employment-white-paper-submission.

[ix] Australian Institute of Health and Welfare, “Housing Assistance in Australia,” Web Report, July 14, 2023, https://www.aihw. gov.au/reports/housing-assistance/housing-assistance-in-australia/contents/households-and-waitinglists#Waiting.

[x] Johnson, G., Scutella, R., Tseng, Y. & Wood, G. (2018): How do housing and labour markets affect individual homelessness?, Housing Studies, DOI: 10.1080/02673037.2018.1520819

[xi] AIHW. (2021). Specialist homelessness services annual report 2020–21, from https://www.aihw.gov.au/reports/homelessness-services/specialist-homelessness-services-annual-report/contents/clients-services-and-outcomes

[xii] Judith Yates, “Why Does Australia Have an Affordable Housing Problem and What Can Be Done About It?: Why Does Australia Have an Affordable Housing Problem and What Can Be Done?,” Australian Economic Review 49, no. 3 (September 2016): 328–39, https://doi.org/10.1111/1467-8462.12174.

[xiii] Roger Wilkins et al., “The Household, Income and Labour Dynamics in Australia Survey: Selected Findings from Waves 1 to 29” (Mlebourne: Melbourne Institute, 2021).

[xiv] Orsetta Causa and Jacob Pichelman, “Should I Stay or Should I Go? Housing and Residential Mobility across OECD Countries?,” OECD Economics Department Working Papers, vol. 1626, OECD Economics Department Working Papers, October 21, 2020, https://doi.org/10.1787/d91329c2-en.

[xv] Wilkins et al., “The Household, Income and Labour Dynamics in Australia Survey: Selected Findings from Waves 1 to 29.”

[xvi] United States Census Bureau, “Current Population Survey Annual Social and Economic Supplement,” 2022, https://www.census.gov/programs-surveys/cps/data/data-tools.html.

[xvii] Longview and PEXA, “Private Renting in Australia – A Broken System,” Whitepaper 2 (Sydney, 2023), https://longview.com.au/hubfs/Private-renting-in-Australia-a-broken-system-LongView-PEXA-Whitepaper.pdf.

[xviii] Boris Cournede, Sarah Sakha, and Volker Ziemann, “Empirical Links between Housing Markets and Economic Resilience,” OECD Economics Department Working Papers, vol. 1562, OECD Economics Department Working Papers, July 26, 2019, https://doi.org/10.1787/aa029083-en.

[xix] Longview and PEXA, “Private Renting in Australia – A Broken System.”

[xx] Ibid

[xxi] Li, A., Baker, E., & Bentley, R. (2022). Understanding the mental health effects of instability in the private rental sector: A longitudinal analysis of a national cohort. Social Science & Medicine, 296. doi:https://doi.org/10.1016/j.socscimed.2022.114778

[xxii] Barker and Tofts-Len, “Employment White Paper Submission.” 2023, https://www.ceda.com.au/ResearchAndPolicies/Research/Workforce-Skills/Employment-white-paper-submission.

[xxiii] Productivity Commission, “In Need of Repair: Tha National Housing and Homelessness Agreement,” Study Report, 2022, https://www.pc.gov.au/inquiries/completed/housing-homelessness/report.

[xxiv] Benedict, R., Gurran, N., Gilbert, C., Hamilton, C., Rowley, S., & Liu, S. (2022). Private sector involvement in social and affordable housing. AHURI final report no. 388. doi:10.18408/ahuri7326901

[xxv] AIHW. (2022). AIHW National Housing Assistance Data Repositor

[xxvi] Yunho Cho, Shuyun May Li, and Lawrence Uren, “Stamping out Stamp Duty: Property or Consumption Taxes?” (Canberra: Centre for Applied Macroeconomic Analysis, Crawford School of Public Policy, ANU, 2021).

[xxvii] Barker and Tofts-Len, “Employment White Paper Submission.” 2023, https://www.ceda.com.au/ResearchAndPolicies/Research/Workforce-Skills/Employment-white-paper-submission.

[xxviii] NSW Treasury, “NSW Property Tax Proposal” (Sydney: NSW Government, 2021), https://www.nsw.gov.au/sites/default/files/2021-06/property-tax-progress-paper-june-2021.pdf.

[xxix] Michael Warlters, “Stamp Duty Reform and Home Ownership,” Economic Record, July 26, 2023, 1475-4932.12754, https://doi.org/10.1111/1475-4932.12754.

[xxx] Cavelleri, M. C., Cournede, B., & Ozsogut, E. (2019). How responsive are housing markets in the OECD? National level estimates. Paris: OECD Economics Department Working Papers No. 1589. doi:https://dx.doi.org/10.1787/4777e29a-en

[xxxi] Adalet McGowan, M., & Andrews, D. (2015). Skills mismatch and public policy in OECD countries. Paris: OECD Economics Department Working Papers No. 1210. doi:https://dx.doi.org/10.1787/5js1pzw9lnwk-en

[xxxii] de Boer, R., & Bitetti, R. (2015). A Revival of the Private Rental Sector of the Housing Market?: Lessons from Germany, Finland, the Czech Republic and the Netherlands. Paris: OECD Economics Working Paper No. 1170. doi:http://dx.doi.org/10.1787/5jxv9f32j0zp-en

[xxxiii] Fred Hanmer and Michelle Marquardt, “New Insights into the Rental Market” (Sydney: RBA and ABS, 2023), https://www.rba.gov.au/publications/bulletin/2023/jun/pdf/new-insights-into-the-rental-market.pdf.

[xxxiv] Rachel Ong et al., “Demand-Side Assistance in Australia’s Rental Housing Market: Exploring Reform Options,” AHURI Final Report, no. 342 (October 29, 2020), https://doi.org/10.18408/ahuri8120801.

[xxxv] Productivity Commission, “In Need of Repair: Tha National Housing and Homelessness Agreement.” Study Report, 2022, https://www.pc.gov.au/inquiries/completed/housing-homelessness/report.